Spain: Championing High-Growth Hospitality and Living Opportunities

After several years of exceptional performance and near-record investment volumes, Spain remains one of the most compelling hotel markets in Europe. But the Spanish market in 2026 is no longer simply a story of recovery and growth. It is increasingly a story of capital intensity, product transformation and strategic repositioning.

On March 25th at 08:15h, I will have the pleasure of moderating a roundtable discussion at the International Hospitality Investment Forum (IHIF EMEA) in Berlin, where we will explore these trends in depth. Below is a brief overview of where the Spanish hospitality market stands today.

1. Performance

Operationally, 2025 confirmed the extraordinary strength of the Spanish hotel sector. According to the STR and Cushman & Wakefield Hotel Barometer, Spain closed the year with record operating levels:

– ADR: €166.1 (+4.8%)

– RevPAR: €125.4 (+5.5%)

– Occupancy: stable at historically high levels (+0.7%)

The story of 2025 was therefore one of quality over volume, with pricing power continuing to drive performance growth.

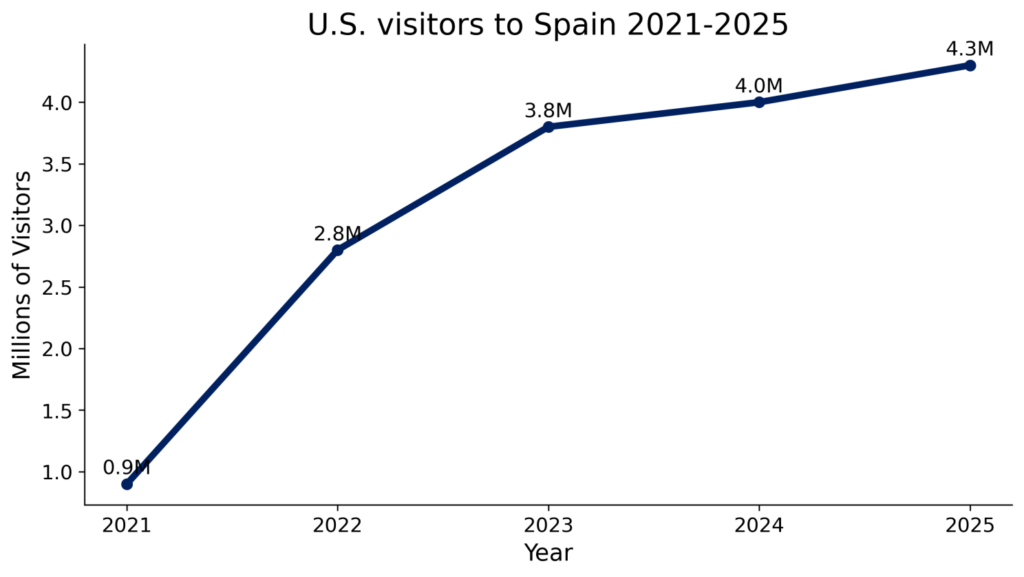

Source: Atout France, INE, NTTO

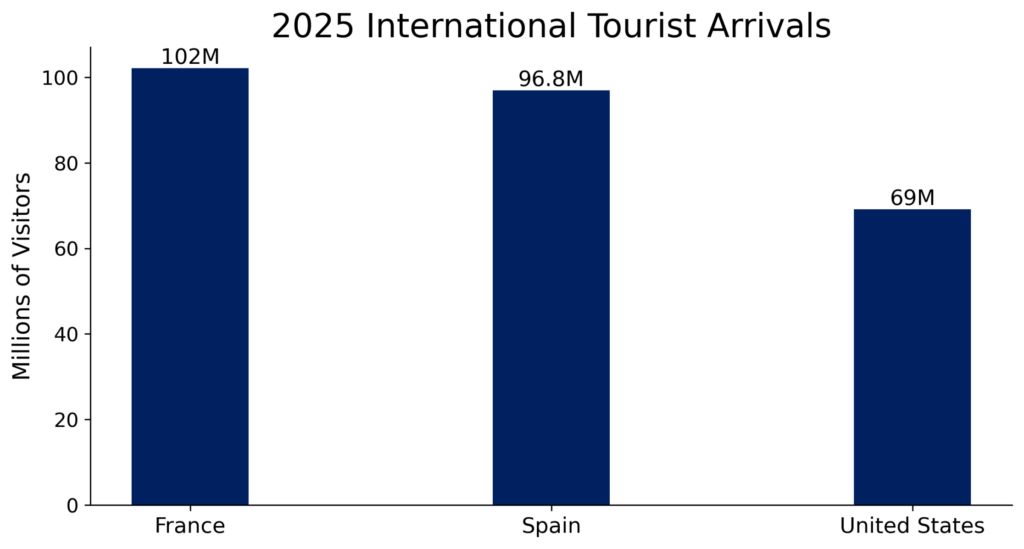

At the macro level, Spain continued to benefit from strong international tourism flows, consolidating its position as the second most visited country in the world.

2. Investment & development

From an investment perspective, Spain remained one of the most attractive hotel markets in Europe in 2025, combining strong liquidity with record transaction volumes:

– €4.2 billion in hotel transactions, making Spain the second largest hotel investment market in Europe, according to CBRE.

– Institutional capital and hotel operators accounted for 83% of investment activity, according to Christie & Co.

– Hotels represented approximately 24% of total real estate investment, making hospitality the leading asset vertical in Spain, according to Colliers.

Hotel development in Spain remains active but selective. Growth is driven primarily by:

– Asset repositioning

– Brand conversions

– Urban regeneration projects

– Resort upgrades

Unlike previous cycles, development today is largely fundamentals-driven, rather than speculative. The development pipeline is shaped as much by planning constraints and land-use regulations as by investor appetite.

3. Structural themes

Several structural trends continue redefining the Spanish hospitality landscape.

a) Pricing power over volume

Recent years have demonstrated that value creation in Spain is increasingly driven by:

– ADR growth

– roduct repositioning

– Brand strategies

– Active asset management

…as opposed to occupancy growth.

Source: Frontur

b) Hospitality and residential convergence

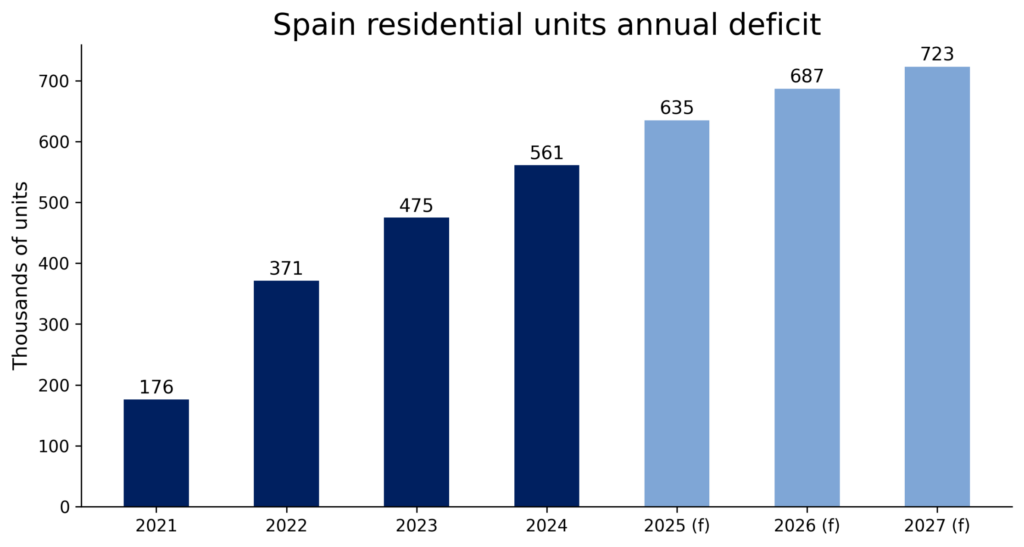

One of the most significant developments in Spain’s real estate market is the growing overlap between hospitality and residential products.

An estimated shortage of approximately 600,000 residential units, according to the Banco de España, is pushing institutional investors toward alternative residential formats, particularly:

– Co-living

– Flex-living

This trend is increasingly visible in projects where residential-style products are developed on hotel land and under hotel licenses, allowing developers to overcome zoning constraints while responding to strong demand for medium-term accommodation.

Source: BBVA Research

At the same time, extended-stay and serviced-apartment operators have expanded aggressively across Spain in recent years.

These operators are reshaping hotel real estate economics in two fundamental ways:

– By generating higher lease levels for owners

– By benefiting from the regulatory pressure on STR units in the hands of individual owners

c) Segmentation and differentiation

Product extremes continue to outperform, and investment activity shows continued polarization between segments:

– Luxury and upper upscale

– Lifestyle and boutique

– Budget and limited service

– Resort all-inclusive

– Alternative hospitality models (extended stay, co-living, hostels)

This increasing segmentation is also revealing a significant repositioning opportunity among traditional commodity 4-star properties, many of which no longer fully match evolving demand patterns.

In summary, the objective of our working session at the International Hospitality Investment Forum (IHIF EMEA) will be to explore these issues together with investors, owners, operators and advisors active in the Spanish market. Some of the questions we will address include:

– Are Spanish hotel assets still underpriced relative to fundamentals, or already fully valued?

– Is ADR growth sustainable, or are we approaching a pricing ceiling?

– Will flex-living/co-living and extended stay absorb capital that previously went into hotels?

– Are traditional hotel operators losing ground to extended-stay platforms?

– Are lease economics being permanently reset by ‘automated’ operators?

If you are considering gaining exposure to the Spanish market, please register here at IHIF to join this roundtable: www.ihifemea.com